They Said It Couldn’t Happen—But the Senate Just Dropped the Big One

Already at the beach for your summer vacation? Pay attention for a moment – taxes are changing.

Permanent 100% Bonus Depreciation

Yes, permanent. Not five years. Not a phase-out. Just a full send from the Senate Finance Committee, among many other big-ticket items, tucked into the latest OBBBA draft.

But before we jump to conclusions, here’s what you need to know:

This isn’t the law yet. The Committee just released its text. The final bill? Still miles away. There’s plenty of negotiating left, especially around SALT caps and IRA energy credits.

Let’s take a look at what’s in it now… and what it means for your planning.

Business Provisions: The Heavy Hitters

100% Bonus Depreciation — PERMANENT

Let’s not bury the lead: The Senate version makes Bonus Depreciation permanent for assets placed in service and acquired after January 19.

No phaseout. No sunset. Just a wide-open door until Congress decides otherwise.

This has broad support — economists, business owners, and even politicians are behind it. Compare it to the House version, which offers only five years. The Senate isn’t just countering; they’re going all in.

§179 Expensing — No Changes, Still a Win

Same as the House version:

- Expensing up to $2.5M in equipment purchases

- Phaseout starts at $4M

This aligns nicely with the 100% depreciation policy but is invaluable for investors who don’t qualify under bonus depreciation.

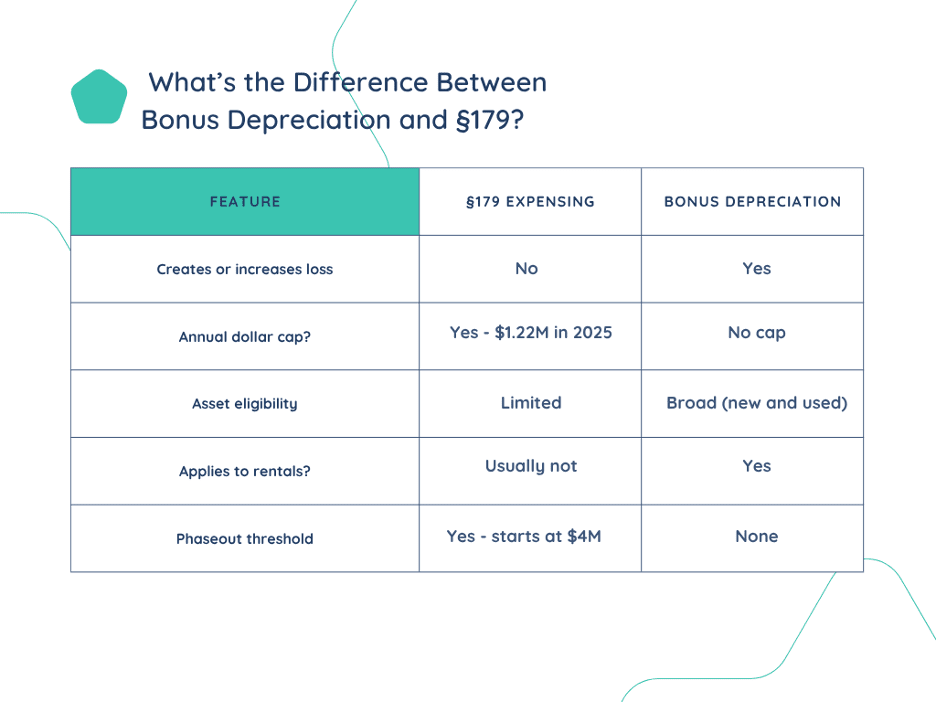

For Those Who Are Confused: Bonus Depreciation vs. §179

Here’s the no-fluff breakdown:

Translation:

- §179 is excellent if you’re profitable and buy equipment up to $2.5M.

- Bonus is the nuclear option—no cap, no profit required.

Still unsure how to play these tools together? That’s what we’re here for.

Interest Expensing – Friendlier Than Ever

The Senate’s version moves the calculation from EBITDA to EBIT. Translation?

You can now deduct more interest because you no longer have to add back depreciation and amortization. That increases your deduction threshold.

Bottom line: more flexibility, especially for capital-heavy businesses.

Qualified Small Business Stock (QSBS) Expansion — Quiet, But Major

This flew under the radar:

The exclusion for QSBS jumps from $10M to $15M — and it’s now indexed to inflation.

What is QSBS?

QSBS stands for Qualified Small Business Stock, a tax exemption under Section 1202 of the IRS Code. If you hold stock in a qualifying business for five years, you can potentially exclude the gain when you sell, up to:

- $10 million, or

- 10x your investment (whichever is greater)

Now, the Senate wants to raise that cap to $15M, indexed for inflation. That’s a serious upgrade for founders, early employees, and investors.

Pass Through Entity Tax (PTET) Deduction — Tweaked, Not Deleted

No full repeal like I expected. SSTB restrictions are gone, but they’ve installed a cap:

- You can deduct the lower of $40K or 50% of your original deduction.

Feels more like a patch job than real reform, but it’s not a loss either.

Qualified Business Interest Deduction — Locked in at 20%

If you were hoping for 23%? Not happening.

But here’s the silver lining:

The 20% QBI deduction is now permanent, and that matters.

No expiration date to plan around. Just consistent, reliable tax planning for pass-through businesses.

Individual Provisions: Here’s What’s In (and What’s Not)

What’s Locked In:

- Individual Tax Rates

- Standard Deduction

- Child Tax Credit (Increased)

- Gift Exclusion (Increased)

No Tax on Tips

Up to $25K ($50K if married filing jointly), phased out at $150K AGI. This benefit sunsets after 2028. Not as broad as hoped, but still a win for service workers.

No Tax on Overtime

This is up to $12.5K ($25K MFJ) and will end in 2028. It’s limited, but it’s something.

SALT Cap — Still the Spiciest Issue

The Senate isn’t happy. They floated $0 as a starting point. The current $10K cap isn’t sticking, but no one expects a return to the $40K limit.

Personal take:

Mortgage and SALT deductions probably shouldn’t exist, but let’s be real — they’ll likely land around $25K, with a phaseout. Want to argue? Buy me a cocktail.

Expect fireworks as this one gets hammered out.

Timeline Reality Check

This is just the Senate Finance Committee’s draft. Before it becomes law, it still has to:

- Survive markup

- Get through the Budget Committee

- Pass the full Senate

- And then, get reconciled with the House

That July 4th goal? Not happening

Earliest I’d bet on? Labor Day. Maybe.

But here’s the good news:

90% of this bill is aligned. The last 10%? That’s where the real fight will be.

The Bad News for Business Owners…

When 100% Bonus Depreciation becomes permanent, every business owner and their cousin will knock on their CPA’s door like it’s Black Friday at a Best Buy.

Spoiler alert: That’s not the time to start asking tax questions.

Let’s talk now if you’re considering making big moves this year, buying equipment, investing in growth, or just wanting to keep more of your earnings. Beat the rush. Be smart.

Book a free discovery callbefore my calendar looks like a Costco parking lot.

Be A Financial Olympian™,

Michael Tannery, CPA, Creative Thinker

(Still accepting clients who know the early bird gets the full deduction)